| Name | Capital Small Finance Bank Unlisted Shares |

|---|---|

| Sector | Banking |

| Security Type | Pre-IPO/Unlisted Equity Shares |

| Face Value | ₹ 10 |

| ISIN Code | INE646H01017 |

| Available in Depository | CDSL & NSDL |

| Capital Small Finance Bank Unlisted Share Price | Now Listed |

| Lot Size | - |

| Minimum Investment | ₹ 42000-48000 |

| All Time High | ₹ 460 |

| All Time Low | ₹ 200 |

| Highlights | - Diverse Portfolio with high proportion of secured lending - Strategic presence in North Indian States |

| PAN | AABCC3632Q |

Capital Small Finance Bank commenced operations as India’s first small finance bank in 2016, and are among the leading SFBs in India in terms of asset quality, cost of funds, retail deposits and CASA deposits for Fiscal 2021. (Source: CRISIL Research Report).

Capital Small Finance Bank has the most diversified portfolio with sizeable book in multiple asset classes as compared to other SFBs with a highest proportion of secured lending of 99% as of Fiscal 2021 among the SFBs. (Source: CRISIL Research Report).

Capital Small Finance Bank has the best asset quality among the SFBs represented by lowest GNPA and NNPA of 2.08% and 1.13% respectively as of Fiscal 2021. Further,

Capital Small Finance Bank has the highest CASA ratio of 40% in Fiscal 2021 as compared with other SFBs and are amongst the top 10 banks vis a vis the private sector banks. (Source: CRISIL Research Report).

Capital Small Finance Bank also has the highest retail deposits per branch of `322.50 million as of Fiscal 2021. (Source: CRISIL Research Report) and have the lowest cost of funds among the SFBs as of Fiscal 2021. (Source: CRISIL Research Report)

Capital Small Finance Bank has an experience of over two decades in the banking industry having operated as the largest local area bank prior to their conversion into a small finance bank. (Source: CRISIL Research Report) They are one out of the two non-NBFC microfinance entity to receive the SFB license in 2015 (Source: CRISIL Research Report).

The core strategy of Capital Small Finance Bank is to build a robust retail focused banking franchise by enabling access to affordable credit in the states they operate with special emphasis on rural and semi-urban areas. they focus primarily on the middle-income customer segments i.e., customers with an average annual income of `0.4 million to `5 million.

Capital Small Finance Bank targets to be the primary banker to their customers and endeavour to achieve objective through a mix of (i) suite of their product offerings; (ii) customer service orientation; (iii) deeply entrenched physical branch network ; and (iv) evolving digital channels of service delivery.

CASA deposits as on June 30, 2021 and March 31, 2021 were Rs.22,194.46 million and Rs.20,926.34 million representing a CASA ratio of 40.48% and 40.07%, respectively of Capital Small Finance Bank, which is the highest among the SFBs for Fiscal 2021 resulting in lowest cost of deposits among peers at 5.7%.

(Source: CRISIL Research Report).

Capital Small Finance Bank operates on a branch-based model. Headquartered in Jalandhar, Punjab, they have over the years expanded their SFB operations strategically in the north Indian states of Punjab, Haryana, Rajasthan and Delhi where they offer their banking services in a contiguous manner.

Capital Small Finance Bank have the highest branch network in the state of Punjab as compared to any other SFBs and fourth largest when compared with the private sector banks. (Source: CRISIL Research Report).

As of June 30, 2021, Capital Small Finance Bank were present in four States with 159 branches and 161 ATMs with 74% of their branches located in rural and semi-urban areas covering 19 districts and 77.35% of their total customers (both credit and deposit).

Source – Capital Small Finance Bank DRHP

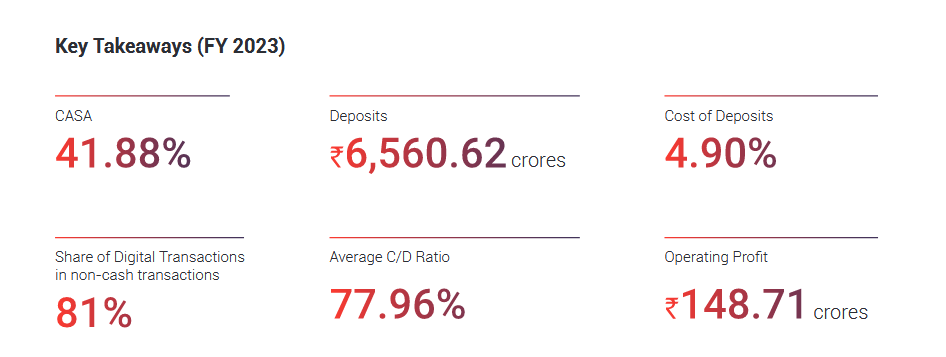

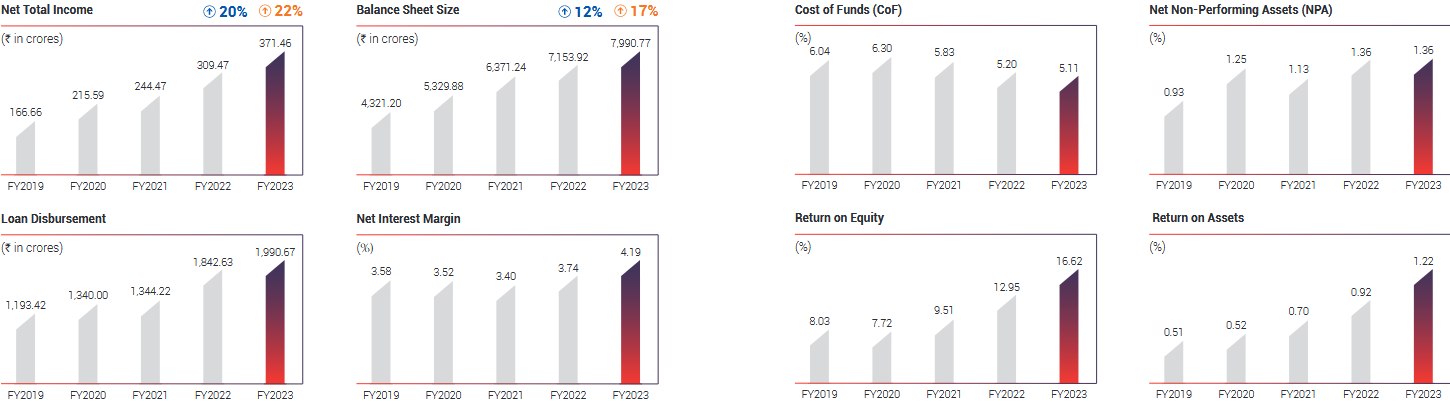

Capital Small Finance Bank Key Highlights FY23:

Source: Capital Small Finance Bank Annual Report FY 2022-23

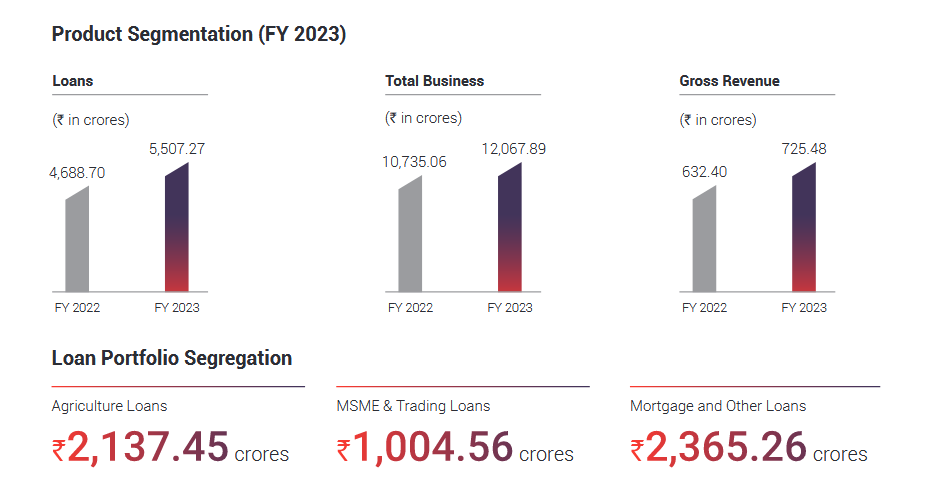

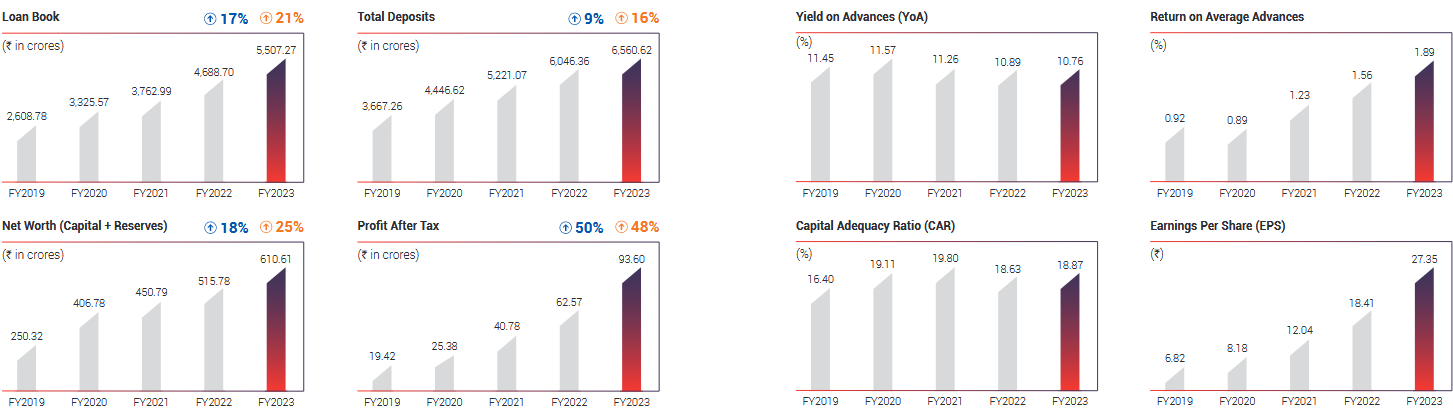

Operational & Financial Performance:

Source: Capital Small Finance Bank Annual Report FY 2022-23

Key Investors in Capital Small Finance Bank:

Key Partners in Capital Small Finance Bank:

Source: Capital Small Finance Bank Annual Report FY 2022-23

| Particulars | FY 2022-23 | FY 2021-22 | FY 2020-21 |

|---|---|---|---|

| Interest Earned | 676 | 578.21 | 511.43 |

| Other Income | 49.47 | 54.18 | 45.83 |

| Total Income | 725.48 | 632.40 | 557.27 |

| Interest Expended | 354.02 | 322.93 | 312.82 |

| Operating Expenses | 222.75 | 196.25 | 172.95 |

| Provisions and Contingencies | 55.10 | 50.64 | 30.70 |

| Total Expenses | 631.88 | 569.83 | 516.48 |

| Net profit for the year | 93.59 | 62.56 | 40.78 |

| Profit brought forward | 167.02 | 126.28 | 98.77 |

| Total Profit | 260.61 | 188.85 | 139.55 |

| EPS (In INR) | 27.35 | 18.41 | 12.04 |

*Rates mentioned in the chart are indicative.

The trend indicator above has been derived from the current demand/supply of Capital Small Finance Bank Unlisted Shares. The trend has a tendency to change anytime depending on the market conditions and other events. This indicator must not be construed as any recommendation to buy/sell/hold.

Total Number of Outstanding Shares: 3,42,52,454 (As per Capital Small Finance Bank Annual Report 2022-23)

Market Cap Scenarios:

At 300 Rs/Share, Capital Small Finance Bank Unlisted Shares values the company at approx. Rs. 1,027 crores.

This are just pre-defined scenarios, since the market cap is variable to price, you can calculate the latest market cap based on the ongoing rates of Capital Small Finance Bank unlisted shares.

At 400 Rs/Share, Capital Small Finance Bank Unlisted Shares values the company at approx. Rs. 1,370 crores.

This are just pre-defined scenarios, since the market cap is variable to price, you can calculate the latest market cap based on the ongoing rates of Capital Small Finance Bank unlisted shares.

At 500 Rs/Share, Capital Small Finance Bank Unlisted Shares values the company at approx. Rs. 1,712 crores.

This are just pre-defined scenarios, since the market cap is variable to price, you can calculate the latest market cap based on the ongoing rates of Capital Small Finance Bank unlisted shares.

| Name | Listing Status |

|---|---|

| Arohan Financial | Unlisted |

| AU Small Finance | Listed |

| Equitas Small Finance | Listed |

| Fincare SFB | Unlisted |

| Five Star Business Finance | Unlisted |

| ICL Fincorp | Unlisted |

| Ujjivan Small Finance | Listed |

| Utkarsh Coreinvest | Unlisted |

Capital Small Finance Bank Dividend Declared:

No information found for Capital Small Finance Bank Bonus Issue

No information found for Capital Small Finance Bank Rights Issue

No information found for Capital Small Finance Bank Buyback

Process of Buying Capital Small Finance Bank Unlisted Shares

Get connected with us and inquire for the Capital Small Finance Bank Unlisted Shares

We will quote the current prevailing market rates of the Capital Small Finance Bank Unlisted Shares (Subject to availability)

If you agree on the rate and quantity, we will send our bank details. (Please note, we accept payment only through bank)

Buyer transfers the fund in our bank account and buyer also need to send their demat details (for initiating share transfer process)

Post receiving funds and demat details, we initiate transfer of Capital Small Finance Bank unlisted shares. The shares usually gets transferred on same/next working day in your demat account

For detailed buying process, refer here

The minimum lot size for investing in Capital Small Finance Bank Unlisted Shares is 100 Shares

The Lock-in period for Capital Small Finance Bank Unlisted Shares will be Six Months. The Lock-in period starts from the date of IPO allotment. (According to DRHP)

As per the SEBI guidelines, lock-in period for Pre IPO shares is six months. The lock-in period starts from the date of allotment of IPO. During the lock-in period, the shares remain in your account but are marked as locked. After six months, the shares automatically gets unlocked and one can sell it normally on stock exchanges like any other listed shares

Yes, buying Capital Small Finance Bank Unlisted Shares is completely legal

You can regularly check the Capital Small Finance Bank Share Price at our Website and on our Telegram Channel

The IPO of Capital Small Finance Bank can be expected in very short term. The company has already filed its DRHP with SEBI

At Unlisted Arena, you can buy Capital Small Finance Bank Unlisted Shares and many such Pre IPO Shares easily at most reasonable rates with a hassle-free process. Unlisted Arena is India’s leading dealer in Unlisted & Pre IPO Shares

You can sell Capital Small Finance Bank Unlisted Shares:

Before IPO: You can sell Capital Small Finance Bank Unlisted Shares before IPO too. You need to have a buyer for this shares. We can also help you to liquidate your holdings of unlisted shares.

After IPO: Once the lock-in period is complete, you can sell the shares on stock exchanges(NSE/BSE) just like any other listed shares

There are two methods to transfer Capital Small Finance Bank Unlisted Shares

Method 1 – Offline Transfer

In this method, you must have a Delivery Instruction Slip (DIS) book which is provided by your broker. All the demat broking companies have its own DIS book. Along with DIS, there is an annexure which is to be submitted by the seller. Annexure too is provided by the demat broking company. After filing DIS and annexure, duly signed by the seller, they are to be handed over to your respective broker. Post that, your broker will process the request and transfer the shares as per details provided

Method 2 – Online Transfer

One can also transfer shares online through E-DIS/Off Market share transfer. The client must check with their respective brokers if they provide such facility. One can also transfer shares through CDSL easiest (for CDSL Demat) and NSDL Speed-E (For NSDL Demat) after registering into it

Yes, Capital Small Finance Bank Unlisted Shares are in demat form just like listed shares. You can buy and store them in your demat account. Like listed shares, Unlisted Shares also have their ISIN code so that you can verify the authenticity of shares

Once the process is complete, Capital Small Finance Bank Unlisted Shares will reflect in your demat account. The shares usually gets reflected in your Depository holdings (DP Holdings). You can check it in your stock brokers app/website. The shares are also shown on your DP transactions and holding statement.

You can also check your holdings in the following:

If you have CDSL Demat Account – CDSL Myeasi app

If you have NSDL Demat Account – NSDL Speed-E

Many investors do ask ‘How to buy Capital Small Finance Bank Unlisted Shares in Zerodha, Angel One, Upstox, etc?’

You can buy Capital Small Finance Bank in any demat account with any broking company

When it comes to delivery of unlisted shares- Be assured as Unlisted Arena is the fastest in delivering shares. Once the process is completed, we usually deliver the shares on same day or the next working day. i.e T day or (T+1) working day

Short Term Capital Gains Tax: If unlisted shares are sold in 24 months or less, gains from such sale are taxed at the slab rate

Long Term Capital Gains Tax: If unlisted shares are sold after holding for more than 24 months, gains on such sale will be taxed at 20% after indexation

Tax on Capital Gains on Unlisted Shares that are sold after getting listed: The tax rates will be the same as that on purchase and sale of listed shares.

That is, the long-term gains (shares sold after holding for more than one year) will be taxed at 10% after a threshold of ₹ 1 lakh per financial year.

Short-term gains (gains on selling shares in one year or less) will be taxed at 15%

You can check the historical price trend by checking Capital Small Finance Bank Unlisted Shares price graph here Capital Small Finance Bank Unlisted Shares price chart will help you get an idea about price-action. You can also check the current trend of Capital Small Finance Bank Unlisted Shares here

For listed shares, there are numerous applications and website which shows the market capitalization of shares. But no need to worry, we have included market capitalization scenarios on our website which shows market cap/valuations of the company based on prevailing Unlisted Shares rates. In addition, we have also mentioned total number of shares so that you can easily calculate current market cap quickly without putting much efforts. Click here to see the valuations of Capital Small Finance Bank Pre IPO shares

Quick tip: Market Cap= Total Outstanding shares x Price per share

You can easily check latest developments, news related to Capital Small Finance Bank Unlisted Shares on our website without any sign up or login. Click here to know about latest news and happenings

Unlisted Arena is a prominent name which facilitates Unlisted Shares & Pre IPO Shares safely and securely. All the transactions are done through bank accounts where no third parties are involved. Unlisted Arena always quotes transparent rates and is also known for its fastest delivery of Unlisted Shares and Pre IPO Shares. Unlisted Arena gets featured regularly in India’s top most financial publications. You can check media coverage of Unlisted Arena here

Capital Small Finance Bank is a Pre IPO company. Capital Small Finance Bank has plans to get its stock listed on exchanges. For that purpose, Capital Small Finance Bank has already filed its DRHP with SEBI

Yes, NRIs can also buy and sell Capital Small Finance Bank Unlisted Shares just like domestic investors. But their investment is on a non-repatriable basis

Like any listed shares, Unlisted Shares price is also determined by demand-supply of Unlisted Shares. Higher the demand, higher the price and vice-versa. The rates of Unlisted Shares are also derived from its performance, corporate actions such as declaration of results, bonus, dividend, etc. Another important aspect is share price/valuation of its listed peer. If the listed business is identical, unlisted companies share price/valuation will too be in similar fashion

At Unlisted Arena, we charge Zero Brokerage/Charges. The rates quoted by us are- net rates, i.e., you do not need to pay any brokerage or charges

One can buy Capital Small Finance Bank Unlisted Shares in any demat account – no matter with which broker you have a demat account. There is no need for separate/special demat account for buying Unlisted Shares

Unlisted Arena sources Capital Small Finance Bank Unlisted Shares from existing investors looking to liquidate their investment

Yes, you are eligible to get dividend, bonus and/or any other corporate actions declared by the company. You need to hold the Unlisted Shares in your demat account on the record date declared by the company to be eligible for such corporate actions

Copyright 2022 @ Unlisted Arena. All rights reserved.